What is the Factory Automation Market Overview - Definition, scope, and significance?

The Factory Automation (FA) market encompasses technologies, systems, and services that enable the automated control of manufacturing processes. It includes programmable, fixed, and flexible automation solutions, as well as hardware, software, and a range of control technologies such as PLCs, DCS, SCADA, and HMIs. The scope extends across major industry verticals—including automotive, food and beverages, oil and gas, general manufacturing, and mining—providing end‑to‑end integration from machine level to plant level. Automation is significant because it drives productivity, reduces labor dependency, enhances product quality, and enables real‑time data acquisition for smarter decision‑making, positioning FA as a cornerstone of Industry 4.0 and digital transformation strategies worldwide.

What are the Factory Automation Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the relentless pursuit of higher efficiency, labor cost pressures, and the need for flexible production lines to meet customized demand. Technological advances in IoT, AI, and edge computing further accelerate adoption. Restraints stem from high initial capital outlay, integration complexity, and cybersecurity concerns. Challenges involve skill gaps in managing sophisticated automation stacks and legacy equipment retrofits. Opportunities arise from expanding automation in emerging economies, the shift toward collaborative robots (cobots), and the growing demand for predictive maintenance solutions that leverage data from PLCs, DCS, and SCADA systems.

What are the current Factory Automation Market Growth Trends?

Current trends highlight a migration from fixed to flexible automation, allowing manufacturers to reconfigure lines quickly for new product variants. There is heightened adoption of cloud‑enabled HMI interfaces that provide remote monitoring. Integration of AI-driven analytics with SCADA platforms is enabling real‑time optimization. Moreover, the convergence of robotics with programmable automation is blurring traditional segment boundaries, creating hybrid solutions that improve throughput while maintaining safety standards.

How has COVID‑19 impacted the Factory Automation Market and what is the recovery trajectory?

The pandemic exposed vulnerabilities in manual labor‑intensive operations, prompting many firms to accelerate automation projects to ensure continuity amid lockdowns. Initial demand slowed due to supply‑chain disruptions, but once factories reopened, spending rebounded strongly as companies pursued resiliency. The recovery trajectory is positive, with a clear shift toward automation as a risk‑mitigation tool, feeding into the projected CAGR of 8.45% through 2032.

Who are the major competitors in the Factory Automation Market and what is the level of market consolidation?

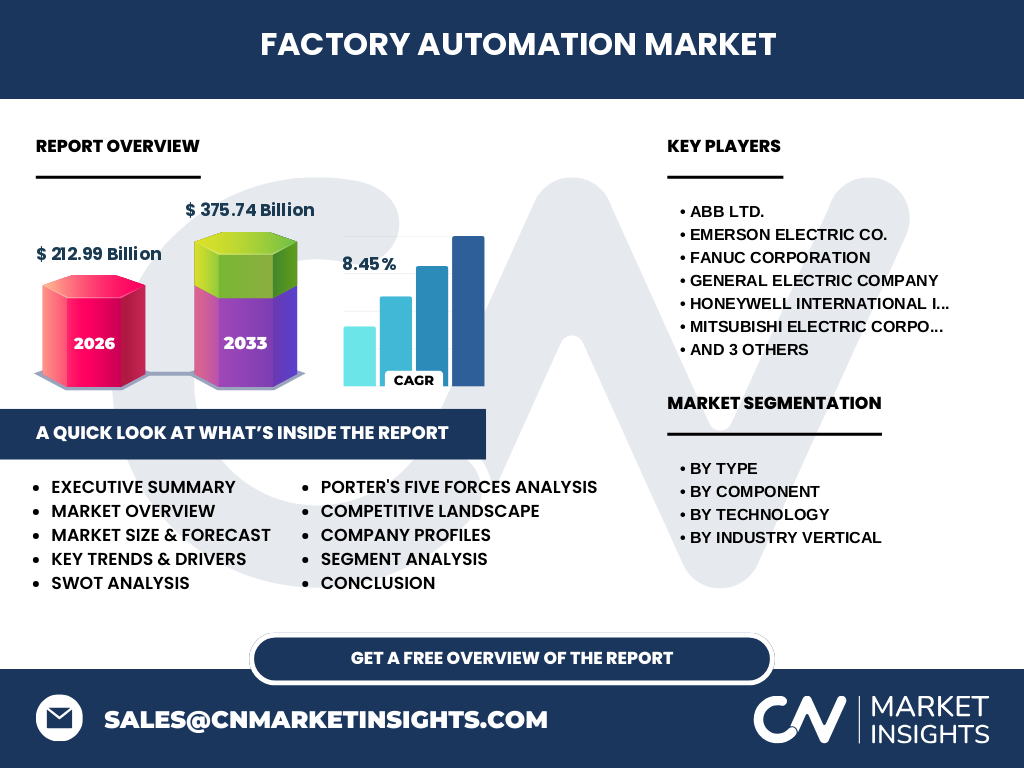

Leading players include ABB Ltd., Emerson Electric Co., Fanuc Corporation, General Electric Company, Honeywell International Inc., Mitsubishi Electric Corporation, OMRON Corporation, Rockwell Automation, Inc., and Siemens AG. The market exhibits moderate consolidation, with these incumbents commanding substantial brand equity, extensive service networks, and integrated product portfolios that span hardware, software, and control technologies. Strategic alliances and acquisitions are common as firms seek to broaden their digital offering and enter new verticals.

What does the Executive Summary reveal about the Factory Automation Market?

The executive summary underscores a robust market valued at US 212.99 billion in 2026, with a forecasted rise to US 375.74 billion by 2033, reflecting an 8.45% CAGR. Growth is fueled by efficiency imperatives, digital transformation, and post‑COVID resiliency strategies. The market is diversified across automation types, components, technologies, and verticals, with North America, Europe, and Asia‑Pacific leading adoption. Competitive dynamics are defined by innovation, service integration, and strategic partnerships among the top nine firms.

What are the Factory Automation Market Forecasts for 2025‑2032?

Based on the provided trajectory, the market is expected to expand from the 2026 baseline of US 212.99 billion to US 375.74 billion by 2033. Applying the 8.45% compound growth rate, the market will consistently outpace many adjacent manufacturing sectors, indicating sustained investment in programmable, fixed, and flexible automation solutions, as well as in the supporting hardware, software, and control technologies.

How is the Factory Automation Market sized and shared by segmentation?

The market segmentation breaks down as follows:

By Type: Programmable Automation, Fixed Automation, Flexible Automation.

By Component: Hardware and Software.

By Technology: Programmable Logic Controller (PLC), Distributed Control System (DCS), Supervisory Control and Data Acquisition (SCADA), Human Machine Interface (HMI).

By Industry Vertical: Automotive, Food & Beverages, Oil & Gas, Manufacturing, Mining.

Each segment contributes to the overall market value, with programmable automation and PLC technology historically representing the largest shares due to their broad applicability across verticals.

What is the Global Factory Automation Market size and share by region?

While exact regional monetary values are not disclosed, the market’s global footprint is anchored by strong adoption in North America, Europe, and the rapidly expanding Asia‑Pacific region. These regions collectively account for the majority of the US 212.99 billion 2026 market, driven by high levels of industrial investment, advanced manufacturing infrastructure, and supportive regulatory environments.

What does the Regional Analysis of the Factory Automation Market reveal?

North America leads with mature automation ecosystems and a focus on advanced robotics and AI integration. Europe emphasizes sustainability and Industry 4.0 standards, fostering growth in flexible automation. Asia‑Pacific shows the fastest growth rate, propelled by large manufacturing bases in China, India, and Southeast Asia, and increasing capital allocation toward modernizing legacy plants. Emerging markets in Latin America and the Middle East present nascent yet promising opportunities.

Who are the leading companies in the Factory Automation Market and what are their strategies?

The top ten firms—ABB, Emerson, Fanuc, GE, Honeywell, Mitsubishi Electric, OMRON, Rockwell Automation, and Siemens—pursue strategies such as expanding digital service portfolios, investing in AI‑enabled control systems, forming joint ventures for vertical‑specific solutions, and acquiring niche technology providers. Emphasis on end‑to‑end solutions that combine hardware, software, and cloud services is a common thread, aimed at locking in long‑term contracts and recurring revenue.

How does Porter’s Five Forces analysis apply to the Factory Automation Market?

Threat of New Entrants: Moderate, due to high R&D costs and established brand equity of incumbents.

Bargaining Power of Suppliers: Low to moderate; component suppliers (sensors, semiconductors) have some leverage, but large manufacturers often source globally.

Bargaining Power of Buyers: Increasing, as large OEMs demand customized, integrated solutions and can negotiate volume discounts.

Threat of Substitutes: Low, because automation offers unique productivity gains not easily replicated by manual processes.

Industry Rivalry: High, driven by technological innovation, service differentiation, and geographic expansion.

What are the SWOT highlights for the Factory Automation Market?

Strengths: Proven ROI, scalability, and alignment with Industry 4.0.

Weaknesses: High upfront costs and integration complexity.

Opportunities: Expansion in emerging economies, AI‑driven predictive maintenance, and collaborative robotics.

Threats: Cybersecurity risks, rapid technology obsolescence, and potential trade barriers affecting component supply.

What does the Factory Automation Market Value Chain analysis show?

The value chain starts with raw material suppliers (electronics, sensors), moves to component manufacturers (PLC, HMI), system integrators that design and install automation solutions, and ends with end‑users (manufacturers). After‑sales services, upgrades, and data analytics form a critical post‑implementation layer, generating recurring revenue and fostering long‑term customer relationships.

What key investment insights can be drawn for the Factory Automation Market?

Investors should focus on companies with strong software and services capabilities, as these drive higher margins and recurring income. Targeting firms that are expanding in Asia‑Pacific or forming strategic partnerships in high‑growth verticals (e.g., electric vehicle manufacturing) can yield superior returns. Monitoring M&A activity will also reveal consolidation trends and potential upside for early‑stage technology players.

What conclusions can be drawn from the Factory Automation Market analysis?

The market is on a clear growth trajectory, underpinned by an 8.45% CAGR and a projected increase to US 375.74 billion by 2033. Automation is transitioning from cost‑center to strategic enabler, delivering resilience, efficiency, and data‑driven insights. Companies that innovate across hardware, software, and services while addressing cybersecurity and skill development will capture the greatest market share.

How was the research methodology for this report conducted?

The study employed a mixed‑method approach: primary interviews with industry executives, secondary data extraction from reputable databases, and quantitative modeling to extrapolate future values based on the provided 2026 market size and CAGR. Segmentation was validated through cross‑referencing of technology adoption rates and vertical‑specific reports.

What is the scope of this research and its limitations?

The research covers global Factory Automation markets across type, component, technology, and industry vertical dimensions, focusing on the top nine market participants. Geographic coverage includes major regions but does not detail individual country‑level financials due to data availability. Forecasts extend to 2033, assuming the continuation of current macro‑economic and technological trends.

Which key companies and recent developments are shaping the Factory Automation Market?

Key players such as ABB, Siemens, and Rockwell Automation have launched next‑generation PLC platforms with integrated edge analytics. Fanuc announced a partnership with a leading AI firm to embed machine‑learning capabilities into its robot controllers. Mitsubishi Electric introduced a cloud‑based HMI suite for remote plant monitoring. OMRON expanded its sensor portfolio to support higher‑precision applications in automotive assembly. These developments illustrate the market’s shift toward smarter, more interconnected automation ecosystems.